Global Art Market Trends 2026

Global Art Market Trends 2026

Insights from the Art Basel & UBS Art Market Report and the Australian Auction Market

The global art market sits at the intersection of culture, finance, and international trade. Each year the Art Basel & UBS Global Art Market Report provides one of the most comprehensive assessments of the international art trade, drawing on data from galleries, auction houses, collectors, and financial institutions to map the direction of the global market.

The 2026 report, authored by cultural economist Dr Clare McAndrew of Arts Economics, indicates that the art market entered a period of renewed growth during 2025 after two years of contraction. Global art sales increased by approximately four percent, reaching an estimated US$59.6 billion. While this represents a return to positive momentum, the market remains slightly below the peak levels recorded in 2022.

Rather than signalling rapid expansion, the data suggests a phase of stabilisation. Collectors remain active, yet the market has become increasingly selective, with demand concentrating around works of strong provenance, institutional recognition, and historical significance.

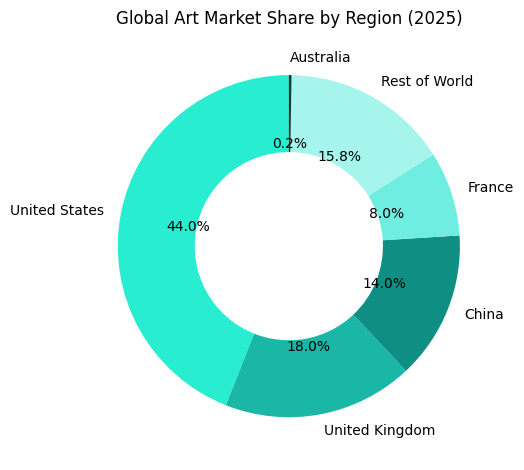

The United States remains the largest art market, followed by the United Kingdom and China. Together these three regions account for approximately 76 percent of global art market value, underscoring the continued concentration of activity within a small number of financial centres.

Key Market Figures

Global Art Market 2025

US$59.6 billion in sales

Auction Market Growth

+9 percent year-on-year

Dealer Market Growth

+2 percent year-on-year

Online Art Sales

US$9.2 billion (approximately 15 percent of the market)

Australian Auction Market

A$149.5 million in sales during 2025

Sources: Art Basel & UBS Art Market Report 2026 and compiled Australian auction data.

The Structure of the Global Art Market

Despite the globalisation of the art trade over recent decades, market activity continues to be concentrated within a small number of financial and cultural centres.

The United States, the United Kingdom, and China collectively account for approximately 76 percent of global art market value, reinforcing their status as the dominant hubs of international art commerce. The United States alone represents roughly 44 percent of total market share, supported by a deep collector base, a sophisticated gallery infrastructure, and the world’s most active auction houses.

London remains Europe’s principal art market centre, while China continues to play a central role in the Asian market despite recent economic volatility.

This concentration highlights an important characteristic of the art market: although artworks circulate globally, the financial mechanisms that underpin their trade remain heavily centralised.

Auction Market Recovery

Public auctions were a major driver of market growth during 2025. Auction sales increased by approximately nine percent year-on-year, outperforming the overall market and reflecting renewed confidence among consignors.

Several major private collections entered the market during the year, and the number of artworks achieving prices above US$10 million increased noticeably. These high-value transactions continue to play a disproportionate role in shaping overall market performance.

This concentration at the top end of the market is a long-standing characteristic of the art trade. During periods of economic uncertainty, collectors often gravitate toward artists with established reputations, museum representation, and strong secondary-market records.

The Role of Galleries

While auction houses experienced stronger growth, the gallery sector expanded more gradually.

Dealer sales increased by approximately two percent globally, reflecting a cautious environment for retail art transactions. Rising operational costs continue to present a significant challenge for galleries, particularly in relation to art fair participation, international shipping, and staffing.

Despite these pressures, galleries continue to dominate the art market as a whole. They account for roughly 58 percent of global art sales, compared with 42 percent for auction houses. Their role in representing artists, shaping careers, and establishing long-term cultural value remains fundamental to the structure of the art ecosystem.

Art Fairs and Collector Engagement

Art fairs have fully re-established their importance following the disruptions of the pandemic years.

In 2025, art fairs accounted for approximately 35 percent of gallery sales, highlighting their continued role as major meeting points between collectors, artists, and galleries. Events such as Art Basel, Frieze, and TEFAF remain essential fixtures within the global art calendar, providing opportunities for collectors to encounter works in person and for galleries to expand their international networks.

While online viewing rooms and digital platforms remain important tools, the highest-value transactions in the art market still rely heavily on physical engagement with artworks.

The Australian Art Market

Although global art-market commentary often focuses on developments in New York, London, and Hong Kong, the Australian art market operates as a distinct regional ecosystem with its own collectors, institutions, and cultural dynamics.

Auction data provides one of the clearest indicators of activity within the Australian secondary market.

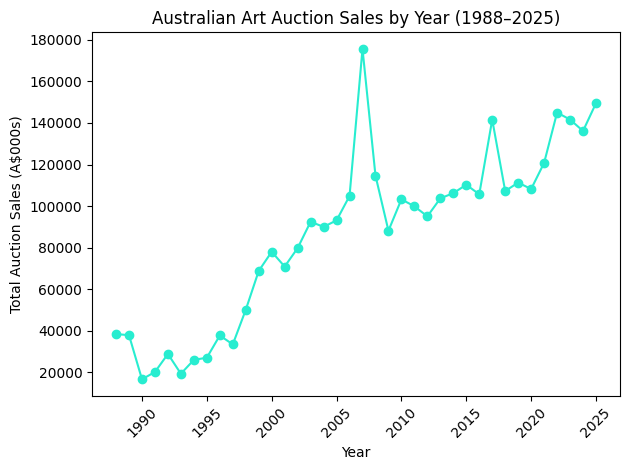

Over the past four decades the Australian auction sector has experienced several cycles of growth and contraction. During the late 1990s and early 2000s, collector interest in Australian modern painting expanded rapidly. Annual auction turnover increased from approximately A$50 million in 1998 to more than A$90 million by 2005.

The market reached a historic peak in 2007, when total auction sales climbed to roughly A$175 million. Like most financial markets, the art sector experienced a significant contraction following the Global Financial Crisis, with auction turnover falling to around A$88 million by 2009.

In the years that followed the market gradually stabilised.

Total auction sales across major Australian auction houses. The market expanded rapidly in the early 2000s, peaked in 2007, contracted following the Global Financial Crisis, and has stabilised around A$140–150 million in recent years.

Australian Auction Sales 1988–2025

Figure 1. Australian Art Auction Sales (1988–2025). Source: compiled from major Australian auction houses including Deutscher and Hackett, Leonard Joel, Menzies, and Smith & Singer.

Recent figures indicate a relatively stable market structure.

Total Australian auction sales reached approximately:

2023 — A$141.6 million

2024 — A$136.1 million

2025 — A$149.5 million

While modest in global terms, these figures demonstrate the resilience of the domestic market.

The Australian Auction Market Today

A relatively small number of specialist firms dominate Australia’s secondary art market.

Among the leading auction houses are:

Deutscher and Hackett

Smith & Singer

Menzies

Leonard Joel

Together these companies form the central infrastructure through which works by major Australian artists circulate between collectors.

The market continues to be anchored by artists with strong institutional recognition, including Sidney Nolan, Brett Whiteley, Arthur Boyd, John Olsen, and Emily Kame Kngwarreye. Works of high quality by these artists consistently attract strong interest when they appear at auction.

At the same time, the secondary market has increasingly broadened to include artists associated with later developments in Australian contemporary art. Figures such as Howard Arkley have seen particularly strong auction momentum in recent years. Arkley’s vivid depictions of suburban architecture and interiors, executed in his distinctive airbrushed style, have become highly sought after by collectors, with major canvases achieving record prices and generating consistent competition at auction.

Other late twentieth-century artists have also consolidated their presence in the secondary market. Painters such as Peter Booth, Tim Storrier, and John Brack continue to attract strong demand, particularly for significant works from key periods of their careers. Storrier’s atmospheric landscape paintings, for example, have achieved some of the highest auction results for contemporary Australian landscape painting in recent years.

More recent contemporary artists have also begun to establish a visible presence within the auction landscape. Works by artists such as Del Kathryn Barton, Ben Quilty, and Daniel Boyd increasingly appear in Australian sales, reflecting the growing institutional recognition and international exposure of their practices. While the markets for these artists remain comparatively young, their inclusion in auction catalogues signals the gradual expansion of the secondary market beyond the traditional modern canon.

This broadening of the market indicates a gradual generational shift within Australian collecting. While historical figures continue to provide the foundation of the secondary market, collectors are also beginning to engage more actively with artists whose careers emerged in the late twentieth and early twenty-first centuries.

ArtVals Market Insight

From a global perspective, the art market appears to be entering a period of recalibration rather than rapid expansion. The strong growth recorded in the immediate post-pandemic years has moderated, and the market now shows clearer signs of selectivity. Activity remains concentrated at the highest price levels, where works with strong provenance, institutional recognition, and established art-historical significance continue to attract competitive bidding. At the same time, the middle segments of the market have become more measured, with collectors demonstrating greater caution and a stronger emphasis on quality.

This pattern reflects a broader structural characteristic of the art market. Unlike many financial markets, art does not move uniformly across all price tiers. Instead, momentum often gathers around a relatively small number of artists and artworks that carry cultural authority and long-term market credibility. During periods of economic uncertainty or adjustment, collectors frequently gravitate toward these works as a form of stability within the market.

Within this broader international context, the Australian art market occupies a smaller yet notably resilient position. While auction turnover in Australia represents only a modest fraction of global art sales, the domestic market has demonstrated a remarkable degree of continuity over time. Supported by a committed collector base, strong institutional collections, and a long tradition of engagement with modern and contemporary Australian art, the secondary market continues to maintain steady levels of activity.

Auction results over the past decade indicate that collector interest in major Australian artists remains consistent. Works by figures such as Sidney Nolan, Brett Whiteley, Arthur Boyd, John Olsen, and Emily Kame Kngwarreye continue to anchor the market and provide a degree of stability within the broader auction landscape. These artists form the historical core of the Australian secondary market and frequently establish benchmark prices that influence wider collecting patterns.

At the same time, the Australian market remains closely connected to international developments. Global economic conditions, currency fluctuations, and the movement of artworks through international auctions all influence domestic market sentiment. As collectors increasingly operate within a global network of galleries, fairs, and auction houses, Australian artworks also circulate more visibly within the wider international art ecosystem.

Taken together, these dynamics suggest that the Australian art market is likely to continue evolving within a framework of cautious stability. While the scale of the market may remain relatively modest in comparison to major global centres, its institutional depth, established collector base, and cultural significance ensure that it remains an important part of the broader international art landscape.

Source

Art Basel & UBS Global Art Market Report 2026, authored by Dr Clare McAndrew, Arts Economics.